Mitsui & Co. Global Strategic Studies Institute

Communications Infrastructure in Emerging Countries: Present Situation and Future Trends

Apr. 8, 2016

Tetsuya Urakawa

Industrial Studies Dept. II, Mitsui Global Strategic Studies Institute

Main Contents

Mobile phones have been increasingly penetrating the lives of people, and emerging countries are no exception. Behind this spread, there is huge investment in communications infrastructure. Private funds have been invested in communication projects in low- and middle-income countries, and the projects from 2000 through the first half of 2015 amounted to USD 839.5 billion in total, far more than the USD 619 billion of investment in electric power. This report provides an overview of the present situation of communications infrastructure in emerging countries with a focus on mobile phones, and also seeks to discern the future direction of this business.

Communications Infrastructure in Emerging Countries: Present Situation and Future Trends

While fixed-line telephones need a network of telephone lines, mobile phones only require the construction of base stations. This difference lowers investment costs for introducing mobile phones, and the penetration of mobile phones has been accelerated in emerging countries where fixed-line telephones are not readily available. Therefore, the penetration rate of mobile phones in emerging countries is positioned as one of the most important indicators for measuring the progress of the development of communications infrastructure. According to the International Telecommunication Union (ITU), a professional body of the United Nations (UN), the mobile phone penetration rate in emerging countries (Note 1 in Table 1) was only 39.1% in 2007, compared to more than 100% in developed countries. However, penetration in emerging countries caught up at an exponential rate and climbed to 91.1% in 2014. This suggests that the Internet, as well as voice calls, has become available to more people in emerging countries. The Internet penetration rate in emerging countries (Note 2 in Table 1) grew from 11.9% in 2007 to 32.4% in 2014, which, in turn, has brought about significant changes in entire societies. Now there are mobile money services including M-PESA, which allow people to remit money in and out of their countries even if they do not have a bank account. The availability of the Internet has also made it possible to distribute agricultural information in rural areas, such as how to use fertilizer, which is helping increase agricultural productivity.

In addition to state-owned local companies, foreign-affiliated companies have also been playing a major role in the process of mobile phone penetration. In particular, European companies, including Telefonica in Spain, Vodafone in the UK, Orange in France, and Telenor in Norway, have a strong presence in emerging companies. In Latin America and Africa, privatization of state-owned companies, as well as liberalization of communication markets with an aim to introduce competitive markets, were promoted from the 1980s through the 1990s, during which restrictions on foreign investment were relaxed. Consequently, foreign-affiliated companies, mostly from the former colonial powers in those continents, aggressively entered the markets. In Brazil, Peru, and Cote d'Ivoire, where communications infrastructure was mainly developed by foreign-affiliated companies, their mobile phone penetration rates exceeded 100%. The rate stands at 73.8% in Kenya, and at 69.8% even in Mozambique, one of the poorest countries in the world. On the other hand, restrictions on foreign investment are hindering the penetration of mobile phones in countries where the markets are dominated by state-owned companies. Ethiopia’s penetration rate remains at 31.5%.

Overall, the penetration rate of mobile phones is more advanced in Asia, including low-income economies where foreign-affiliated companies are operating, at 132.7% in Cambodia, 80.0% in Bangladesh, and 67.0% in Laos. Telenor, as mentioned earlier, is leading the penetration in Bangladesh, while Viettel of Vietnam and other Asian companies have entered the markets in Cambodia and Laos. Meanwhile, mobile phones were rapidly spreading across India, and its penetration rate jumped from 29.5% in 2008 to 73.2% in 2011, but the complexity of different restrictions for 22 different operation areas in the country capped the penetration at 74.5% as of 2015. In China, whose communication market is dominated by three state-owned companies, they developed communications infrastructure as part of their national policy, pushing the mobile penetration rate up to some extent. However, it remains at 92.7%--relatively low considering China’s economic development level. In addition, in Myanmar, where the market had been monopolized by state-owned MPT, its mobile phone penetration rate was no more than 12.8% in 2013. However, the country changed its policy and began to emphasize the development of communications infrastructure, and granted business licenses to two foreign-affiliated companies, Telenor and Qatar’s Ooredoo. Also, a joint venture launched by KDDI and Sumitomo Corporation began participating in the communications business in Qatar in 2014, and foreign capital-led communications infrastructure development boosted the penetration rate there to 54.0% in one year.

Vodafone and Telefonica Seeking Growth in Emerging Countries

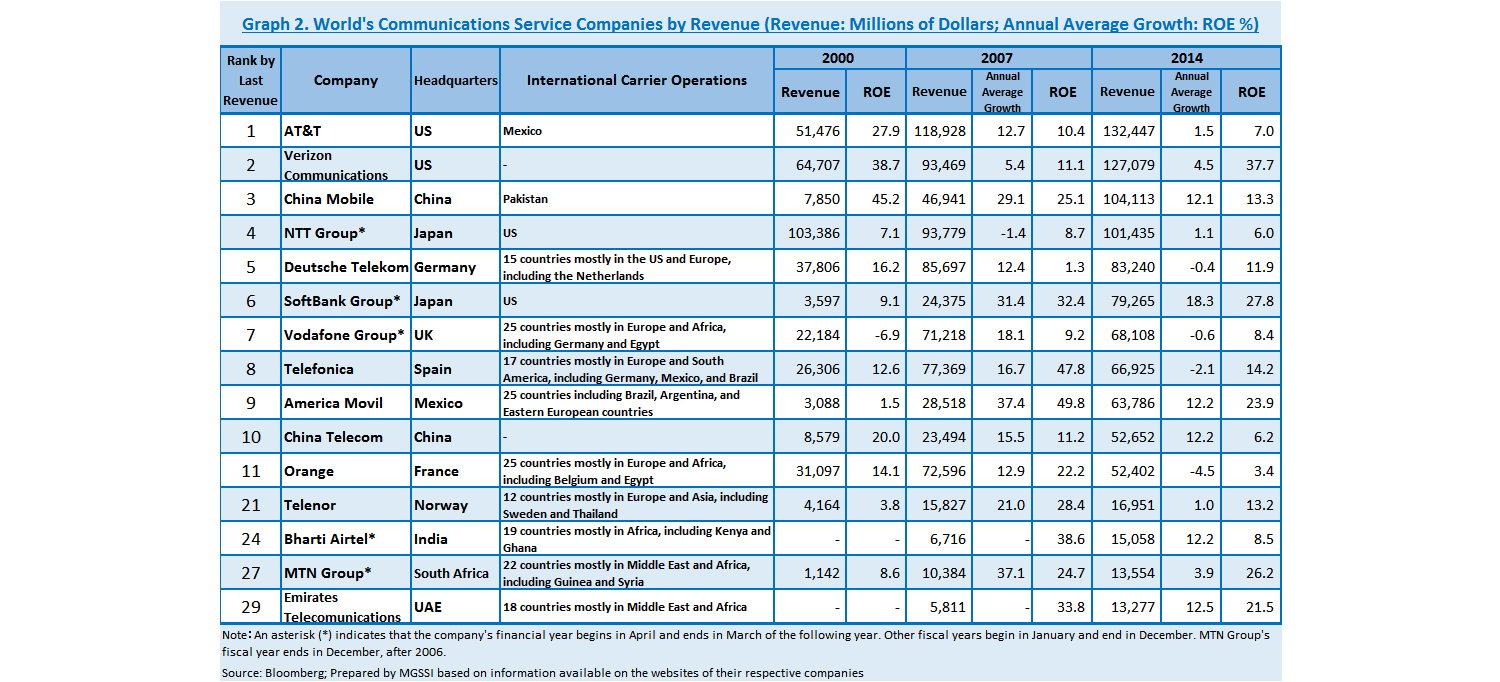

Foreign-affiliated companies have a huge presence in the communications markets in emerging countries. Looking at the revenues of the worldwide communications service companies, the top positions are occupied by companies that survived competition in developed markets and successfully expanded their businesses, including AT&T of the US and Deutsche Telekom of Germany. On the other hand, companies that expanded into emerging countries are in lower positions. (See Graph 2.) European companies, including Vodafone and Telefonica, began operations in emerging countries to secure growth opportunities and avoid intense competition in Europe and developed countries.

Founded in in the UK in 1985, Vodafone began to expand its operations in European countries in 1992. Vodafone was aiming to increase its shares of the domestic UK and European markets, but had to reroute from Europe to other areas for growth opportunities around 2000 because competition with other European companies had become intense. Initially, Vodafone made inroads into Japan and the US, and then withdrew from them due to the severity of competition and the inability to operate under its own brand name. Currently, Vodafone has a presence in a total of 26 countries worldwide, including 13 countries in Europe, and eight countries in Africa, and also India. Telefonica had monopolized Spain’s telecom market until it was liberalized in 1997, and still holds the largest share of the market in Spain. Leveraging its stable revenue and financial strength, Telefonica embarked on aggressive expansion around 1990 centered on Spain’s former colonial sphere of interest, Latin America, and now has a presence in a total of 18 countries, including three in Europe, 14 in Latin America, as well as the US.

Having tapped emerging-country markets, Telefonica and Vodafone engaged in the development of communications infrastructure, then increasing subscribers, and successfully expanded their own operations. In European markets, the average revenue per user (ARPU) has been on the decrease since 2007 while the penetration rate of mobile phones has been growing. However, thanks to business expansion in emerging-country markets, the two companies succeeded in maintaining company-wide growth.

Two Trends and Future Direction

There will be two main trends in communications infrastructure in emerging countries. One is the intensification of competitive environments. Mobile phones are still not prevalent in some emerging countries such as Ethiopia, as well as in some rural areas, leaving room for foreign-affiliated companies to enter and expand into. In particular, Mexico and Myanmar have implemented additional measures for easing foreign investment in recent years, and thus are expected to accelerate the development of communications infrastructure. However, the competition in such emerging markets may, over time, become as severe and mature as that of developed markets. European companies operating in emerging countries have already suffered from price competition, and the boost effect on earnings that they have enjoyed in emerging-country markets is beginning to fade. Moreover, there will be a need for additional investments to improve the quality of communication. A future requirement will be to enhance stability and speed, considering not only voice calls but also data communications via the Internet. That situation may drive foreign operators that cannot bear the additional investment costs out of those countries or towards forming business alliances, as is often the case with developed markets. Meanwhile, businesses will likely be oriented towards diversification by distributing video and music services via the internet, as well as strengthening alliances with non-communications areas including the financial sector. However, the increase in ARPU in low-income emerging countries is expected to reach a limit, and the quality of communications infrastructure is inferior to that in developed countries. Therefore, in order to operate Internet businesses in emerging countries, it may be effective to adopt different technologies and business models from those in developed countries.

The other trend is the rise of emerging-country companies. China Mobile, which acquired China Tietong Telecommunications Corporation in 2008, has been expanding its business by pressing forward with increasing the penetration rate of mobile phones and the Internet within China, to break into the world’s top three in terms of revenue. Also, America Movil of Mexico, Bharti Airtel of India, and MTN of South Africa, Etisalat of UAE, and Zain of Kuwait are expanding overseas aggressively. Viettel has reached not only Asia but also Mozambique and Latin America. America Movil, which originated in the former state-owned TELMEX, has formed an oligopolistic market with an over 70% share in Mexico, enjoying great earning power. Capitalizing on these resources, the company has advanced into foreign countries, especially those in Latin America since 1999, and made inroads into Europe by acquiring Telekom Austria in 2014. Bharti Airtel, a 100% privately-owned company, is India’s largest communications company that provides mobile communications service throughout the country. As mentioned earlier, many telecommunications carriers competed in each of the 22 different business areas in India, which intensified competition. Thus, with overseas expansion in mind, Bharti Airtel acquired Zain’s African operations in 15 countries in 2010, thereby boosting its presence in the African markets.

Competition between European companies and emerging-country companies will widen the coverage of communications infrastructure, improve transmission speed and convenience, and provide low-price service in emerging countries. From a social perspective, this means extending a reach of communications infrastructure to a lower-income population. A new type of BOP (“Base of the Pyramid”) business for the poor will be activated by utilizing communications infrastructure ahead of the manufacturing industry or traditional service industries. The future industrial development process in low- and middle-income countries will be determined largely by the expansion and sophistication of communications infrastructure.