Mitsui & Co. Global Strategic Studies Institute

Growth Potential of Sports Brands and Direction of Their Evolution

Dec. 8, 2017

Yuko Noritake

Industrial Research Dept. II

Mitsui & Co. Global Strategic Studies Institute

Main Contents

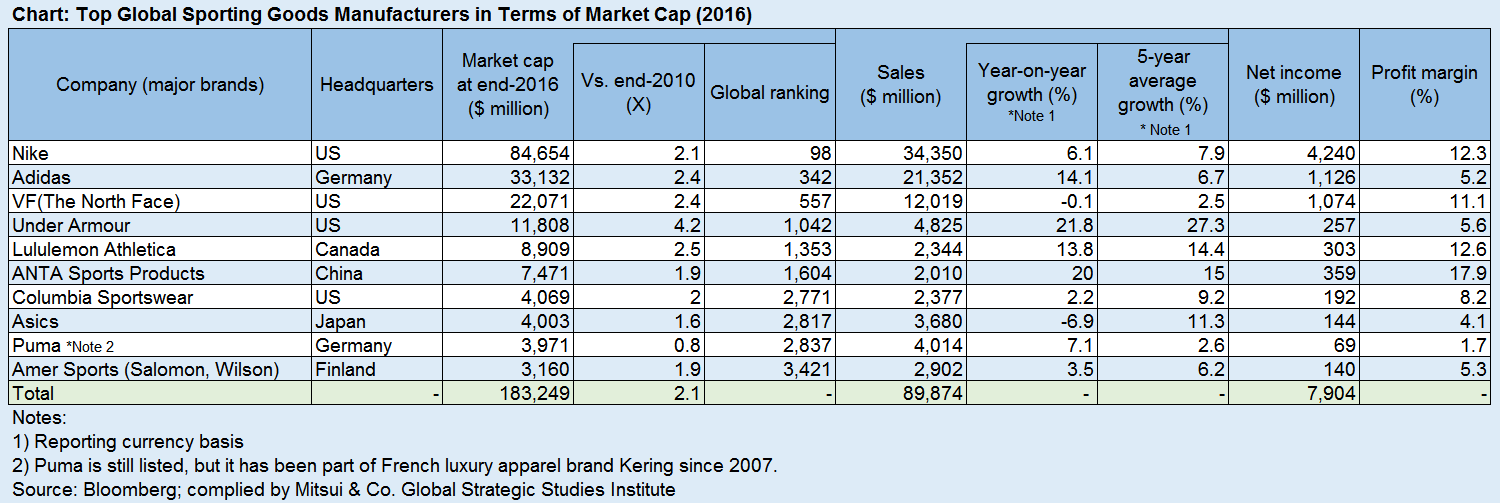

In the stagnant consumer market, particularly in developed countries, sporting goods manufacturers, which develop and manufacture sporting goods and athletic footwear/apparel, are increasingly attracting investors’ attention. As shown in the chart below, the market cap of the 10 leading sporting goods manufacturers, which are ranked among the top 5,000 companies in the world in terms of market cap, surged 2.1-fold on an aggregate basis in the period between the end of 2010 and the end of 2016. The pace of growth easily topped that of 618 consumer goods manufacturers (up 1.6-fold) and that of 82 apparel manufacturers (up 1.5-fold) in the same period, with the latter included in the former. It was nearly equal to the 2.3-fold increase for SPAs (manufacturing retailers in the apparel industry) that have performed particularly well in the apparel industry, including Inditex (mainstay brand Zara) and Fast Retailing (Uniqlo). This report examines factors behind the higher valuation of sporting goods manufacturers, including the operating environment and business models, and looks at the potential of such players.

Growth Potential of Functional Apparel Market

Underlying factors behind the growing interest from investors in sporting goods manufacturers include the rising number of people playing sports, mainly in developed nations, as people become more health conscious. In particular, walking, running, and working out, which are easy to start, are growing in popularity among a wide range of age groups. Demand for functional shoes and apparel, which provide comfort while exercising, is thus increasing.

In addition, sports have become part of many people’s lifestyle in recent years, and shoes and clothing designed for athletic activities are now worn on other daily occasions. This trend is called “athleisure” in the fashion industry, and even those who do not play sports wear such outfits simply because they are cool.

There were some examples in the past where sports apparel turned into fashionable items. A typical example is “polo shirts.” Polo shirts were first worn by polo players, but René Lacoste, the founder of casual fashion brand Lacoste and a famous tennis player, invented a short-sleeved version of polo shirts for tennis and wore it, which caught the public eye. More recently, Nike’s sneakers became all the rage among young people, thanks in part to collaboration with top athletes and popular rappers. Note, however, that this boom was limited to some items and certain age groups.

In contrast, the recent trend in sports clothing being worn in daily life applies to a variety of items and a wider range of buyers, including female and elderly people. As such, the impact on the overall industry and each player will likely be much larger. With this serving as a tailwind, sporting goods manufacturers with a high weighting of shoes and apparel in total sales, such as Nike, Adidas, Under Armour, and Canadian yoga wear brand Lululemon Athletica, have seen particularly robust earnings growth.

Consequently, many major sporting goods manufacturers are now positioned as emerging players in the apparel industry. While SPAs are generally doing well in the industry, those offering reasonable prices and fashionable designs (so-called “fast fashion” items), such as Zara and H&M, are enjoying meaningful growth, while those offering basic and casual fashion items, including Gap, are struggling. In such a casual fashion market, sporting goods manufacturers are growing by taking over existing players’ shares, as their products are favored by consumers due to freedom of movement, comfort, and other characteristics sought in sports clothing. Of note, sporting goods manufacturers can strengthen their brand power by providing top athletes with their footwear and clothing for competitions. Such athletes’ brilliant performance should make a strong impression on consumers and enhance the brand image.

The functional apparel market is expected to continue to expand going forward in both developed and developing countries. Competitiveness in this field could lead to the higher valuation of sporting goods manufacturers.

Key Challenges

Although sporting goods manufacturers are growing on the strength of functional apparel, they are facing two key issues. First, competition with apparel manufacturers is intensifying. In recent years, major SPAs such as Fast Retailing, Gap and H&M have stepped up their efforts to attract consumers by focusing on “athleisure” items. For example, Fast Retailing has provided famous tennis player Kei Nishikori with match wear since 2011, and it has expanded its line of sports and active clothing at its Uniqlo and GU stores. Gap has accelerated the opening of new stores for athletic clothing brand Athleta, which it acquired in 2008. H&M also launched the high-fashion sports collection “For Every Victory” in 2016, which was developed in collaboration with the Swedish Olympic team. Moreover, it was reported that Amazon was tapping some athletic-apparel suppliers to make a foray into private-label sportswear. As such, the competition in casual fashion items inspired by sports is expected to become fiercer.

Second, traditional retail channels are weakening. Despite the tailwind from the increasing popularity of sports, sports retailers are hard hit by the rise of online retailers. A typical example is major US sporting goods retailer Sports Authority filing for Chapter 11 protection in March 2016. Many apparel manufacturers have taken the SPA business model, in which they develop products and market them mainly at their directly-managed stores. Meanwhile, sporting goods manufacturers sell their products at their stores, both online and offline, but the weighting of direct sales in total sales is still low, with about 30% for Nike and Under Armour and around 20% for Puma. For those heavily relying on sales via retailers, the weakening of retailers should be a risk factor. Under Armour has sustained relatively strong growth, but the pace of growth is slowing due to discounts at the retail level amid the intensifying competition.

Direction of Evolution

In response to the above two key challenges, sporting goods manufacturers will likely accelerate their SPA business model by increasing the weighting of direct sales, and strengthen their sales capabilities by conducting unique storefront promotional campaigns. Lululemon Athletica has achieved growth by adopting the SPA business model, with its weighting of direct sales exceeding 90%. The athletic apparel company has successfully captured demand by holding free community events at its stores, in which potential customers can experience yoga and running lessons. Meanwhile, given the fact that retailers selling products mainly at their physical stores are struggling amid the rise of online retailers, some players are wary of increasing the number of directly-managed stores. One of the best strategies going forward will be aiming to become an SPA that mainly sells products at its own website. At present, sales in developed markets account for a large portion of total sales of sporting goods manufacturers. By utilizing the Internet, such manufacturers can cultivate demand in emerging markets.

Another growth strategy is evolution into a brand portfolio business. While the SPA business model has been mainstream in the apparel industry in recent years, some players, including LVMH (which owns multiple luxury brands), has been successful with the “brand portfolio” business model, in which companies try to enhance corporate value by increasing each brand’s value. Puma became part of Kering, which owns luxury fashion brands, including Gucci, in 2007. Under Kering’s brand portfolio strategy, Puma acquired a new customer base, including young women, and saw earnings recover, sharply leading to the recent solid performance of the stock. Among sporting goods manufacturers, VF Corporation (mainstay brands The North Face and Vans), which primarily offers outdoor goods and apparel, Columbia Sportswear (Columbia), and Amer Sports (Salomon and Wilson) have expanded their business by acquiring multiple brands, including those dealing with sports-related apparel/goods. In the future, they may further evolve by adopting LVMH’s business model.

Additional options for further growth include expanding the line of business by utilizing a recognized brand as a sporting goods manufacturer. Many players have already provided fitness applications for smartphones, which support users’ health management by keeping exercise logs and measuring calorie intake. Nike has moved ahead of the pack with Nike+ in such area, but other companies have followed suit. Under Armour acquired developers of calorie calculation application MyFitnessPal and fitness application Endomondo in February 2015. Similarly, Adidas bought the application developer of Runtastic in August 2015, and Asics purchased Runkeeper in 2016, respectively. One of the aims of such moves is collecting personal data from users, such as sleeping hours and the frequency and length of exercising. In addition, such data can be used to offer products and services that fit each user’s preference, physical conditions, and exercise history. Asics also made forayed into the nursing care business by opening day-care facilities for adults specialized in functional training, including exercise programs, in 2014. Mizuno is also expanding its sports facilities and service operations (management of public sports facilities, futsal/tennis courts). By utilizing its brand power, the company offers fitness programs for various age groups and hosts events inviting top athletes to serve as coaches.

Along with health and foods, sports is a key area of “wellness,” a concept attracting attention recently. Nestle, the largest food company in the world, aims to expand its business to the entire wellness field, with its focus on foods. Similarly, sporting goods manufacturers can expand its businesses by enhancing investments into or alliance with firms offering foods and health-related products and services, while focusing on sports. Their brands are highly recognized by consumers, as they are associated with health. As such, sporting goods manufacturers have the potential to become a core part of a wellness conglomerate holding a variety of business. They will likely increase their presence not only in the stock market but also in the real marketplace.