Mitsui & Co. Global Strategic Studies Institute

Can Brazil’s Economy Regain its Strength?

May 10, 2017

Osamu Katano

North America & Latin America Dept.

Mitsui Global Strategic Studies Institute

Main Contents

Brazil’s economy is recovering from a terrible period. Real GDP growth recorded a 3.8% decrease in 2015 over the previous year and a 3.6% decrease in 2016. It was the second consecutive annual negative growth for the first time ever since 1930-31. However, real GDP growth in 2017 is expected to be 0.4% over the previous year, and it is highly likely to show positive growth despite narrow range. The reason why Brazil’s economy has bottomed out mainly stems from the improved sentiment of businesses and households due to the stabilization of the political confusion which brought about the recession, and at the same time the positive effect of the interest rate cut by the Central Bank of Brazil (BCB). Further positive effects from the interest rate cut are also highly expected going forward.

However, the economy is projected to remain consistently sluggish. This is because Brazil has the difficulty of depending on the export of resources under the circumstances of slow global economic growth, and therefore high economic growth is no longer expected. It is also because the weight of Balance Sheet Adjustments, a negative legacy of past overconsumption, still remains in Brazil’s economy. Furthermore, the Temer administration maintains its strong desire to accomplish fiscal reform even at the cost of the economy. Considering these circumstances, it is better to assume there is a likelihood that real GDP will not overcome negative growth in 2017, even though this likelihood is small.

Balance Sheet Adjustments in Brazil

Balance Sheet Adjustments is the mechanism for controlling consumption or investment in order to prioritize the repayment of borrowings (reduction of outstanding debt). During the term when adjusting movement continues, a decline in the interest rate is not immediately reflected in an increase of consumption or expansion of investment. Rather, the economy is more likely to remain sluggish.

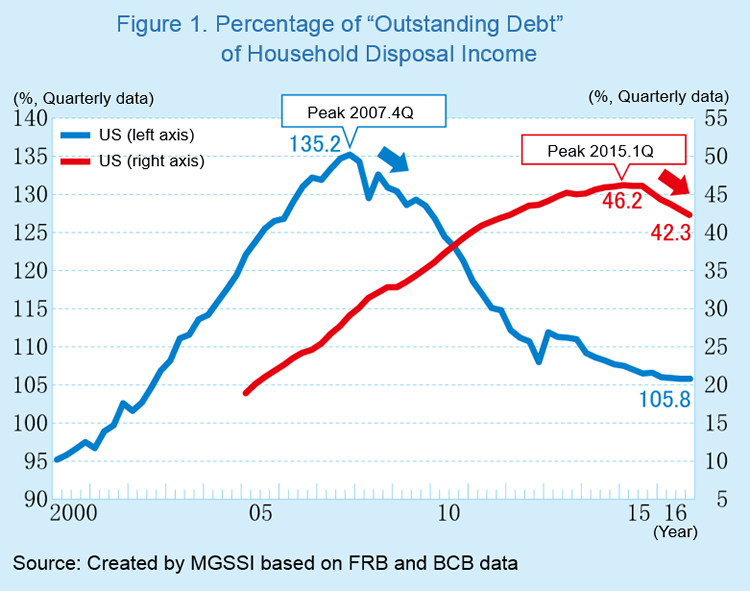

A movement of Balance Sheet Adjustments can be confirmed by the ratio of “Outstanding Debt” or “Repayment Amount of Debt” compared to disposable income. First, since 2005, the expansionary track of outstanding debt in Brazilian households continued until reaching its peak of 46.2% at the beginning of 2015. However, since 2015, its downward trend has been continuing (Figure 1).

In Brazil, the natural resource boom in the 2000s had brought about an appreciation of Brazilian Real, causing the low rate of inflation. These circumstances were followed by a decline in interest rates and the formalization of labor, which led to the realization of expanding access to financial institutions. As a result, households took out loans to expand personal consumption, and thereby outstanding debt has expanded.

However, the demise of the natural resource boom, political confusion due to corruption problems, and the financial reform (tax increase policy) pursued by the Rousseff administration has caused the extreme deterioration in economic conditions. Since 2015, households have been forced to tackle the reduction of the outstanding debt under a situation of sluggish disposable income growth due to the economic slowdown.

When looking at the situation of Balance Sheet Adjustments in Brazil, the example of the U.S. serves as a reference to a certain extent. In 2008, the financial crisis hit the U.S. economy, and as a result, outstanding debt, which had expanded by 1.35 times (135.2%) compared to total household disposable income, had to be reduced. Currently in the US, outstanding debt compared to disposable income has declined significantly (105.8%) since 2008 (Figure 1). However, this ratio has not yet been reversed. That is to say, Balance Sheet Adjustments are seen to be continuing.

The real GDP growth rate in the U.S. during the term of Balance Sheet Adjustments (2009-2016) had an annual average rate of 2.1%. However, the contribution from personal consumption accounts for 1.6% of the above rate, which is lower than that of 2.3% during 10 years (1998-2007, average growth rate: 2.9%) prior to financial crisis. Therefore, this shows that the driving force of personal consumption has been declining.

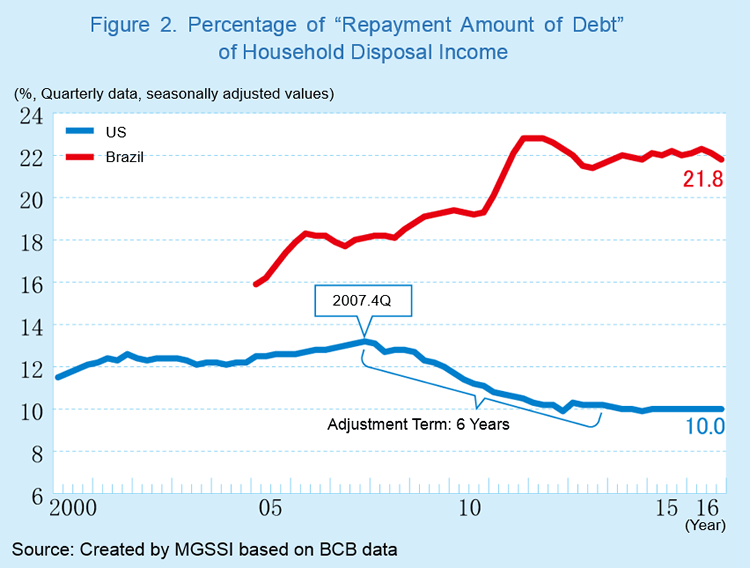

In Brazil, the comparison ratio of the peak value of outstanding debt to disposable income is 46.2%, which is only about one third of the ratio in the U.S. However, what is notable here is the high repayment amount of debt (comparison ratio of disposable income). As for its scale, its recent ratio is 10.0% in the U.S. On the other hand, the ratio in Brazil is 21.8%, which is two times higher than the US figure (Figure 2). On top of that, the point of the problem in Brazil is that half of the amount of the repayment debt is the financial burden of interest payments. In Brazil, where a high interest rate policy has continued to be taken, interest payments account for a high percentage of the repayment amount of debt, and therefore, the pace of reduction of the outstanding debt could be slow considering the heavy burden of the monthly interest payment.

In the U.S., Balance Sheet Adjustments still continue in terms of outstanding debt. In terms of the repayment amount of debt, 6 years of Balance Sheet Adjustments has been a hard time of adjustment. It is conceivable that the Balance Sheet Adjustments which started in 2015 in Brazil will also not likely end in the short term, and might be extended for a long period of time because the monthly repayment amount has been expanding due to the high financial burden of interest payments. Therefore, steps towards economic recovery during this term are projected to be sluggish.

Maintaining the Fiscal Reform Policy despite the Sluggish Economic Recovery

Under such circumstances, the Brazilian government’s consistent efforts towards fiscal reform serve as downward pressure on the Brazilian economy in 2017. From the start of the second Rousseff administration, such governmental efforts started. However, the current Temer Administration, which was established in August 2016, focuses on cuts in expenditures instead of the tax increase policy which the former Rousseff administration adopted, and enacted the constitutional limit of public spending in December, 2016.

This law stipulates that any increase in the Brazilian government’s expenditure budget is to be restricted within the range of the inflation rate during the 12 months up to the previous June. In other words, it sets out that actual increase rate will be negative (calculated by discounting rising prices). In principal, this law will be applied to the budget in the next 20 years, and an increase of 7.2% is set as the cap on the expenditure budget in its draft for Fiscal 2017.

The policy of the Temer Administration can be said to be effective in prioritizing general theory in the process of fiscal reform. This is especially because the Temer Administration has reconstructed its financial condition, starting with the restriction of the total expenditure amount instead of coordination among individual expense items for revenue and expenditure. In fact, the administration is easier to obtain congressional approval by upholding fiscal reform as a goal. On the other hand, citizens as well as members of the congress who are constantly paying attention to citizens’ movement are more likely to oppose the details of the measure for reducing public spending and expanding revenues, preferring to avoid increased burdens or decreased benefits.

Moreover, the Temer Administration’s enthusiasm for fiscal reform is shown in the revised budget of Fiscal 2017 which was released on 29 March, 2017. Initially, the Brazilian government projected the real GDP growth rate as 1.6% compared with the previous year; however, it revised the relevant rate downward to 0.5%, which was close to the market forecast. Because of the change in assumption of revenue due to this revision, a budget deficit of 197.2 billion Brazilian Real, which exceeded the deficit of 139 billion Brazilian Real as the target of the initial fiscal revenue and expenditure (excess of 58.2 billion Brazilian Real), was projected. Therefore, the government announced the revised budget with the combination of a reduction of 42.1 billion Brazilian Real in expenditure and an increase of 16.1 billion Brazilian Real in order to defend the initial target of the primary balance.

These measures are the outstanding examples which show the Temer Administration’s persistence with the policy of fiscal reform. Just continuing to carry through with them might hinder economic recovery. For example, the reduction of expenditure incorporated at this time includes the reduction of 30% of the budget for “Acceleration of Growth Plan (PAC)”, or 10.5 billion Brazilian Real. This reduction alone put downward pressure on GDP growth rate (estimated 0.5% decrease).

Why is Fiscal Reform Focused on Now?

A public opinion backlash against fiscal reconstruction, which has a cooling effect on the economy, is inevitable. However, economic recovery in the mid and long term cannot be expected once financial collapse occurs, even though Balance Sheet Adjustments is completed. President Temer embarked on fiscal reform, recognizing the seriousness of the loss of the qualified investment grade for national bond ratings caused by the past policy of fiscal expansion and fiscal deficits, and the adverse effects of the depreciation of the Brazilian Real due to this downgrade. In addition, Temer clearly fears that the social welfare system cannot be maintained without resolution of the fiscal deficit.

Looking at the current circumstances in Brazil, President Temer is fortunate to be able to aggressively pursue fiscal reform. This is because he can gain the cooperation of other parties by way of demonstrating himself as not standing as a candidate for the next presidential election and adopting an attitude of “taking a personal risk for others” through fiscal reform.

However, the above mentioned expenditure cap method or a temporary reduction for a revised budget does not serve as fundamental fiscal reform. Although the expenditure cap method among others appears to be a powerful measure at first glance, which expenditure items will actually be reduced is left up to future decision.

Under this circumstance, the government undertook “Pension Reform” to restrict the increase of pension benefits which account for more than 40% of the expenditure budget. The Brazilian population aged 65 and over accounts for 9.4% of its total population (estimated by the United Nations in 2020), which is a lower percentage compared with that of advanced countries, and pension benefits account for only about 9 % of GDP. On the other hand, while the Japanese population aged 65 and over accounts for 28.5% of its total population, pension benefits account for only about 6 % of GDP. This is because a system to provide “greater” social welfare, which exceeds that of Japan, has been introduced in youthful Brazil, and not a rapidly aging society like Japan. However, the Brazilian government expects that its social welfare system cannot be maintained under such circumstances. Accordingly, pension reform is a pressing issue.

Parliament Disturbed by Public Opinion Backlash

The government’s pension reform draft, which was announced in December 2016, included a revision to raise the starting age of pension benefits to 65, although in the current pension plan, pension benefits can be received in a person’s 50s. Many people have retired from work in their 50s because they could receive full pension benefits despite a short enrollment period. However, in the future, people will need to work until their mid-60s to maintain their livelihoods. Therefore, recipients will be forced to change their future life plans drastically. As a result, protest activities such as street marches are intensifying.

On 19 April 2017, the government submitted a draft revision to lower the starting age for pension benefits for women to 62, and change the 49 years enrollment period required for full pension benefits to 40 years. However, the response from the national congress has been lukewarm because of the public opinion backlash. Enactment of the said revision draft requires the consent of at least three-fifths of the members of the national congress both in the upper house and the lower house (i.e. 49 upper house members; 308 lower house members). However, less than 100 out of 513 members in the lower house agreed with the said draft.

In 2017, it is expected that Balance Sheet Adjustments will continue and improvement of business confidence will be delayed despite the interest rate cut. In addition, the October 2018 presidential election will come into focus, and thereby promotion of the policy, which forces ordinary voters to accept economic pain, will become more and more difficult as time passes. At the same time, the investigation of several corruption cases, in which many politicians are thought to be involved, will be progressing earnestly, and therefore another public opinion backlash might be further intensified.

Nevertheless, clarifying the path to fiscal reform is imperative for Brazil’s economy to regain its health. It is desirable that President Temer persistently advocates the necessity of fiscal reform to enable pension reform to be implemented by the end of 2017, before the 2018 presidential election campaign gets into full swing.