Mitsui & Co. Global Strategic Studies Institute

Expansion of Electric Vehicles in Europe: Status and Outlook

Nov. 8, 2016

Yoichi Yoshizawa

New Business & Technology Development Center, Mitsui & Co. Deutschland GmbH

Main Contents

With fuel efficiency regulations increasingly tightening year after year, Europe has been striving to promote electric vehicles (“EVs”).1 However, remaining issues, such as driving range, charging time, and price, have been a barrier to EVs gaining popularity. The environment surrounding EVs has been experiencing changes, as represented by the adoption of the Paris Agreement at the United Nations Framework Convention on Climate Change (COP21) in 2015, and the strategy shift of Volkswagen (VW) following the emissions scandal. This report outlines status and policies on EVs in Norway and the Netherlands—two EV pioneers in Europe—as well as France, the UK, and Germany, and also provides an outlook on the future of EVs in Europe.

NORWAY AND THE NETHERLANDS TAKE THE LEAD

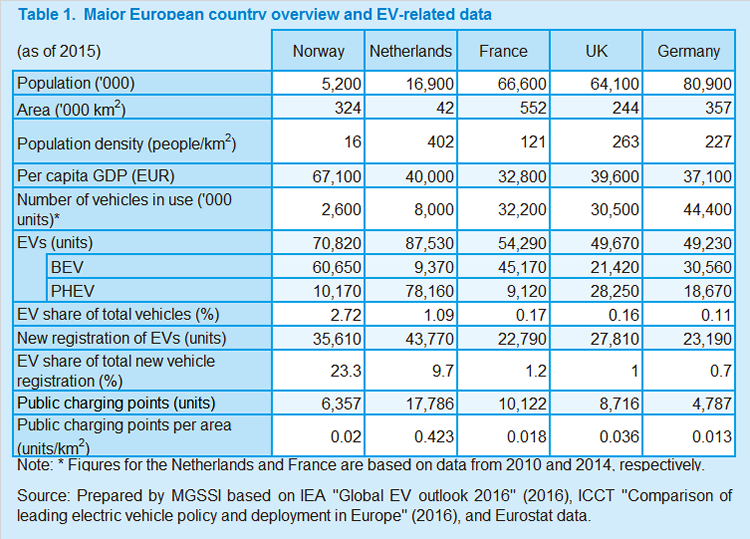

As of the end of 2015, there were approximately 1.26 million EVs worldwide, 30% of which existed in Europe. Table 1 shows EV-related data for major European countries. The most EV-popular country in Europe is Norway. There are 2.6 million passenger cars, of which 70,000 are EVs. This makes up the EV proportion 2.7%, which is the highest in the world. Moreover, one in five new cars registered in 2015 was electric. The popularity of EVs in Norway is shown by the fact that in 2015 VW’s EV e-Golf was the best-selling car of all cars including internal-combustion engine (ICE) vehicles. The biggest factor behind this popularity is the government’s substantial incentives for battery electric vehicles (BEVs). BEV purchasers are exempt from car registration taxes (introduced in 1996) and value-added taxes (VATs) (introduced in 2001). These incentives, coupled with large cuts on car ownership taxes (introduced in 2005), have made EVs more affordable to own than the same model of ICE vehicles. According to a survey study targeting EV buyers, the respondents stated economics as the primary reason for purchasing EVs. BEV users are also entitled to benefits such as exemption from road tolls and free parking in public spaces (introduced in 1997 and 1999, respectively). In fact, Norway has special circumstances; 97% of its power generation is low-cost hydroelectric, allowing the country to focus on reducing CO2 in the transport sector. Moreover, Norway is a wealthy country where many households own two cars. Nevertheless, it is still true that the government’s consistent EV policy2 over two decades is finally taking effect.

In the Netherlands, there are almost 90,000 EVs, or 1.1% of the total passenger cars, which is the second highest after Norway. In 2015, 43,770 new EVs were registered, corresponding to 10% of all registered vehicles. The best-selling EV of the year was Mitsubishi Motors plug-in hybrid electric vehicle (PHEV) Outlander. A car registration tax is imposed according to the amount of carbon dioxide (CO2) emitted, which means that EVs with less CO2 emissions have an advantage. BEVs are exempt from car ownership taxes, which are calculated by vehicle weight. Characteristically, most EVs are owned by companies, as tax incentives (whereby employees who drive a corporate EV pay a lower tax rate) have successfully encouraged businesses to purchase EVs. However, since this tax rate doubled for PHEVs in 2016, partly due to increasing financial burdens on the government, the sales volume of EVs fell to one-half in 2016 from the previous year. Another key factor to success was the commitment of the central government and municipalities to develop public charging infrastructure. In the Netherlands, there are over 17,700 public charging points—more than in Norway. Parking and charging used to be free, but today both are fee-based in line with the spread of EVs.

FRANCE AND THE UK CATCH UP, GERMANY STARTS LATE

France is aiming to put two million low-emission vehicles on the road by 2020, but as of the end of 2015, the number of EVs was 54,290, only 0.17% of the country’s total. One distinctive policy is the “bonus-malus system,” which was introduced in 2008. Under the scheme, a subsidy (bonus) is granted to the purchase of a low CO2-emission car, whereas a tax (malus) is imposed on the purchase of a high CO2-emission car. Also, a subsidy is granted when a low CO2 emission car is purchased to replace a conventional diesel car. Along with the bonus malus system, EV purchasers could receive up to 10,000 euros in 2015.

The UK has no specific EV numerical targets geared towards increasing the adoption of EVs. The country’s main incentives include: (1) a subsidy called the Plug-in Car Grant, which is received at the point of purchase (25% of the car price, up to GBP 5,000), (2) Vehicle Excise Duty based on CO2 emissions, and (3) tax benefits for a company employee using a company car. As with the Netherlands, the UK is committed to the development of electric charging infrastructure by providing subsidies to the preparation of home chargers and public fast-charging infrastructure.

In Germany, the government has set a goal of deploying one million EVs throughout the country by 2020. However, other than a 10-year exemption from car ownership taxes for BEVs registered by 2015, there were few key measures to promote the purchases of EVs. As of the end of 2015, the number of EVs was no more than 50,000 (EV share of 0.11%). In order to expand EVs’ share, the country introduced a subsidy called the "environmental bonus" in 2016. (For an eligible EV price of up to 60,000 euros, BEVs and PHEVs qualify for 4,000 euros and 3,000 euros, respectively)

OUTLOOK THROUGH 2020

In the short term, Norway will remain the leader propelling EVs in Europe. The country continued to see an increasing number of EVs registered in 2016, reaching a cumulative total of over 100,000 units. In particular, PHEV sales have grown rapidly since 2015. Presumably, households who own only one car are buying PHEVs, which cause less range anxiety (the fear that a vehicle has inadequate range to reach its destination) than BEVs. Phasing out or abolishing BEV incentives has been on the Norwegian parliament’s agenda. Given that exemptions from VAT and car registration tax will remain in effect until 2018 and 2020, respectively, EVs are expected to see stable growth for a while. Norway’s goal is that EVs will account for 100% of the total of new vehicle registration by 2025. In line with this aim, it is projected that the number of sales units will be at least 90,000 EVs, and the cumulative total will exceed 400,000 EVs in 2020.

The Netherlands plans to shift the focus of its support measures to general consumers from 2017 onward. The country is coming to a turning point towards the next expansion stage. With charging infrastructure being developed, the groundwork has been laid for the country to have more EVs on the roads.

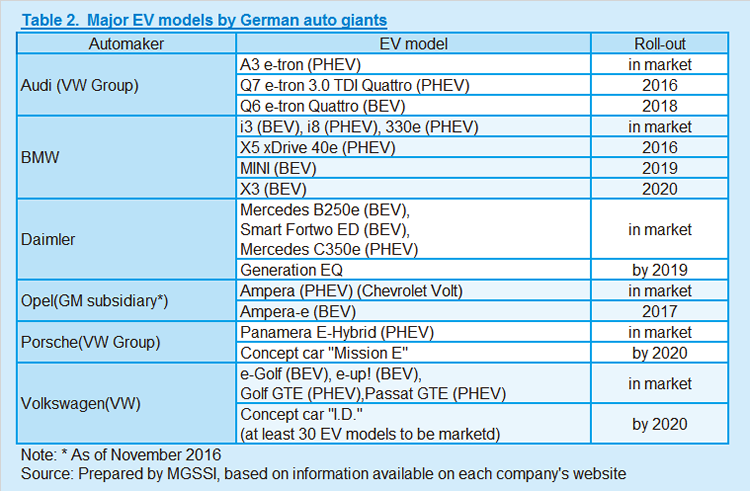

It is likely that EVs will expand gradually in France and the UK, unless there is any significant change in their existing policies. Assuming that the bonus malus system in France and the Plug-in Car Grant in the UK will remain, EV sales in both countries are projected to reach around 100,000 units by 2020. In Germany, given the introduction of the environmental bonus, as well as a series of new EV models to be marketed by German automakers (Table 2), the potential for EV growth is noteworthy. If all subsidies are allocated, there would be at least 400,000 EVs in total in 2020.

MID-TO LONG-TERM OUTLOOK

CGiven the global trend towards accelerating CO2 emission reduction, fuel efficiency standards will be further tightened. Stronger policy to push the expansion of EVs may be put into place, but policy is not the only important factor. Technological advances are crucial as well. While lithium-ion battery prices3 are decreasing, energy density and thus driving range is increasing. In October 2016, a succession of EV models with a range of around 300 km debuted at the Paris Motor Show. In 2020 and beyond, models with a range of over 500 km may hit the road, due to greater battery performance. Lightweighting, or reducing vehicle body weight, is another key factor. BMW i3 BEV and i8 PHEV use carbon fiber reinforced plastic (CFRP). Furthermore, digitization in the transport sector (self-driving, connected cars, or mobility services using them) could encourage the spread of EVs. The Paris-based EV carsharing service Autolib was launched with 250 BEVs in 2011, and quickly grew to offer 4,000 BEVs and about 6,000 charging points in 2016. The service is taking root as a way of mobility for citizens and has expanded to cities such as Lyon and London. In Amsterdam, EV taxis were introduced by US-based Tesla, which has a factory in the Netherlands, and free-floating carsharing service car2go by Daimler, uses its BEVs, Smart Fortwo. In the future, EVs may replace taxis and carsharing in other cities as well.

Ultimately, the expansion of EVs is dependent on consumer acceptance. As shown by the survey in Norway mentioned above, consumers place the highest priority on price. Thus, EVs also need to be price-competitive with ICE vehicles. Bloomberg New Energy Finance (BNEF), a research firm, predicts that by the mid-2020s, lower battery prices and longer driving ranges achieved by enhanced performance could make the total cost of ownership4 of an EV less than that of an ICE vehicle, even without subsidies.

As a leading European automaker describes the spread of EVs as “evolution” rather than “revolution,” it is likely that EVs will be continually and gradually rolled out across Europe, but the level of development will differ depending on the country. Norway will lead Europe in proliferating EVs, followed by the Netherlands, and large countries such as France, the UK, and Germany. Should the current incentives to promote the adoption of EVs remain unchanged, it will be post-2020 that EVs enter a period of expansion in the major markets. By then, the total cost of EV ownership is expected to further decrease. Technological advances such as improving battery performance and lightweighting materials would contribute to acceleration of EVs becoming popular throughout Europe.

- An electric vehicle (EV) includes a hybrid car in a broad sense, but in this report, it is defined as a pure battery EV (BEV) and a plug-in hybrid EV (PHEV).

- Despite the change of administration, incentives for BEVs have been maintained. Other than those described in this report, incentives include access to bus lanes (introduced in 2005) and free access to ferries (introduced in 2009).

- Lithium-ion batteries, which cost nearly USD 1,000/kWh in 2010, fell by half to USD 300-400/kWh in 2015. The cost is expected to drop to more or less USD 200/kWh.

- An aggregate of the purchase price of a vehicle and running costs including automobile insurance premiums, fuel charges, and vehicle inspection fees.

References

- Bloomberg (February 25, 2016). Here’s how electric cars will cause the next oil crisis (retrieved from https://www.bloomberg.com/features/2016-ev-oil-crisis/).

- Bloomberg New Energy Finance (February 25, 2016). Electric vehicles to be 35% of global new car sales by 2040 (retrieved from https://about.bnef.com/blog/electric-vehicles-to-be-35-of-global-new-car-sales-by-2040/).

- European Alternative Fuels Observatory (2016). Retrieved from http://www.eafo.eu/.

- International Council on Clean Transportation (ICCT) (2016). Comparison of leading electric vehicle policy and deployment in Europe (retrieved from http://www.theicct.org/sites/default/files/publications/ICCT_EVpolicies-Europe-201605.pdf).

- International Energy Agency (IEA) (2016). Global EV outlook 2016.

- Figenbaum, E. and Kolbenstvedt, M. (2016). Learning from Norwegian battery electric and plug-in hybrid vehicle users – results from a survey of vehicle owners (retrieved from https://www.toi.no/getfile.php?mmfileid=43161).

- Netherlands Enterprise Agency (2016). Electromobility in the Netherlands Highlights 2015 (retrieved from https://www.rvo.nl/sites/default/files/2016/08/Highlights%202015%20e-mobility%20in%20the%20Netherlands.pdf).

- Norwegian Electric Vehicle Association (2016). Retrieved from http://elbil.no/english/norwegian-ev-policy/.