Mitsui & Co. Global Strategic Studies Institute

China Strong Promotion of Semiconductor Industry-Proactive Approach with Power Devices-

Jun. 7, 2016

Noriyasu Ninagawa

Technology Studies Dept. II,

Mitsui Global Strategic Studies Institute

Main Contents

Introduction —Promoting Domestic Production of Semiconductor Devices Is a Pressing Need in China:

China, “the world’s factory” for electric and electronic equipment, produces about 40% of the world’s liquid-crystal-display televisions (LCD TVs) and 90% of notebook computers. However, the world’s factory is largely dependent on imports for most of its semiconductor devices, which are the core parts of such equipment, with its self-sufficiency rate at a little over 40% as of 20151. According to China Customs Statistics for 2015, China’s imports of integrated circuits (ICs) -- primary semiconductor devices -- amounted to approximately JPY 2.5 trillion (USD 1 = JPY 110), which revealed that ICs are the largest of all sources of drain on China’s national wealth, including oil.

In response to this, in June 2014, the Chinese government issued the “National Guideline for the Development and Promotion of the IC Industry” aimed at promoting domestic production of semiconductor devices. In particular, an “investment fund” formed under this guideline has capital in excess of JPY four trillion, as evidence of the Chinese government’s serious commitment to the nation’s semiconductor industry. This report discusses China’s moves towards promoting the domestic production of semiconductor devices.

China’s Strategy to Develop Semiconductor Industry

To begin with, it was not a few years ago when China embarked on efforts towards domestic production of semiconductor devices. The first big wave occurred around 2000, when, among other events, SMIC (Semiconductor Manufacturing International Corp., a semiconductor foundry company) was founded with a state-owned enterprise being its largest shareholder. Around the same time, a great deal of attention was drawn to events such as the commencement of operation by China’s largest liquid crystal panel supplier BOE (BOE Technology Group) (1999), as well as Lenovo’s acquisition of the PC business of IBM (2004). It was also during this period that telecommunications equipment company Huawei spun off its semiconductor design unit, HiSilicon in 2004. To summarize these moves, development strategies adopted by Chinese semiconductor device manufacturers can be categorized into the following three:

(1) Strategy with huge investment in plant and equipment

This strategy aims to catch right up with the industry’s leader by acquiring a production line equipped with advanced manufacturing technology, as well as securing personnel in charge of supervision and instruction on the production line. This strategy was adopted by BOE and SMIC. Under this strategy, BOE grew to be the world’s third largest company in terms of market share over ten years, but SMIC’s share of the global foundry market has not reached 5% yet, far behind the world’s largest company TSMC (Taiwan Semiconductor Manufacturing Company, with its market share in excess of 50%). Eventually, they had to compete with industry leaders with cutting-edge technology and manufacturing know-how, and it took them quite a long time to acquire a substantial market share.

(2) Strategy with industry leader acquisition

This strategy involves acquiring a foreign manufacturer that has a certain level of market share with semiconductor devices, in order that the purchaser obtains the technology and production capacity possessed by the manufacturer. In 2015, Tsinghua Unigroup, a state-owned enterprise originating from Tsinghua University, attempted to acquire two US companies, hard disk leader Western Digital and the world’s third largest DRAM manufacturer Micron. However, neither of them was successful, reportedly because the US authorities did not approve the deals in order to prevent technological outflow. Thus, it is clear that such acquisition of industrial leaders faces high political barriers.

(3) Strategy with in-house production of final product component parts

This strategy focuses on switching from outsourcing to in-house production of semiconductor devices used in products for which Chinese manufacturers hold high market shares. For example, Huawei uses its subsidiary HiSilicon for its application processor design. The world’s largest railroad vehicle manufacturer, CRRC Corporation, and the electric car manufacturer, BYD, also internally manufacture semiconductor devices used as component parts for their products.

Among the three strategies above, Strategies (1) and (2) appear to have been stymied at this point; however, no decisive failure has been seen in Strategy (3), under which semiconductor device subsidiaries are showing steady growth along with their parent companies.

In particular, many of the manufacturers employing Strategy (3) handle devices that perform current on/off control called “power devices” 2, and in-house production is an effective means to overcome the difficulty of power device development. Among semiconductor devices (Fig. 1), memories use the most advanced miniaturization technology, but the products themselves are standardized. For logic integrated circuits (ICs), circuit design is separated from manufacture; therefore, a manufacturer receives a layout from a circuit design manufacturer, and then manufactures products based on it. That is, for both memories and logic ICs, horizontal specialization – from customer to design to manufacture – is becoming prevalent. On the other hand, power devices involve not only miniaturization, but also a wide range of development items, including voltage endurance, heat resistance, and high-frequency operation, while specifications subtly vary depending on the application of the device. Thus, power devices are high-mix, low-volume semiconductor devices that require thorough reconciliation with customers. In this industry, an effective strategy would be that a final-product manufacturer (customer) produces semiconductor devices in-house, and specializes in the development and manufacture of promising devices with demand expected to grow.

Another possible reason is an issue relating to the supply chain structure. End users require more demanding specifications for a manufacturer positioned further back in the supply chain. This is presumably because final-product manufacturers require device manufacturers to prepare specifications that take account of a “safety factor.” For instance, the RoHS Directive, or the restriction of certain hazardous substances in products within the European Union (EU), specifies the upper limit on the chemical substance content concentration of products placed on the market. However, final-product manufacturers require device manufacturers to meet tougher standards than the upper limit specified by the RoHS Directive, which weighs heavily upon device manufacturers. Then, as in Strategy (3), if the device division is within a final-product manufacturer, the device and assembly division can design final products through elaborate production, and thus the internal device division is unlikely to be subject to the “safety factor” required when outsourcing. This supply chain structure also may have driven less-technological Chinese device manufacturers to seek a means of survival in in-house production.

China’s Direction of Power Device Technology Development – Key Is In-house Production

China is reliant on imports for over 90% of its power devices, and domestic production is significantly lagging. The industry group for semiconductor device manufacturers in China, the China Semiconductor Industry Association (CSIA), in its “IC Industry Development Outlook” released in March 2016, includes power devices in the five key development items to be addressed during its 15th Five-Year plan (2016-2020), and the country and industry are joining forces to promote domestic production. This gives some manufacturers a new perspective on in-house production, and they are seeing growth while enhancing technology.

Zhuzhou CRRC Times Electric, a CRRC Corporation subsidiary, specializes primarily in high voltage power devices for inverters installed on railroad vehicles. As a result of narrowing down technological issues, the company concentrates its development resources on devices called silicon (Si) insulated-gate bipolar transistors (IGBTs) to respond to growing demand. In fact, sales of Zhuzhou CRRC Times Electric doubled in FY 2015 from FY 2011.

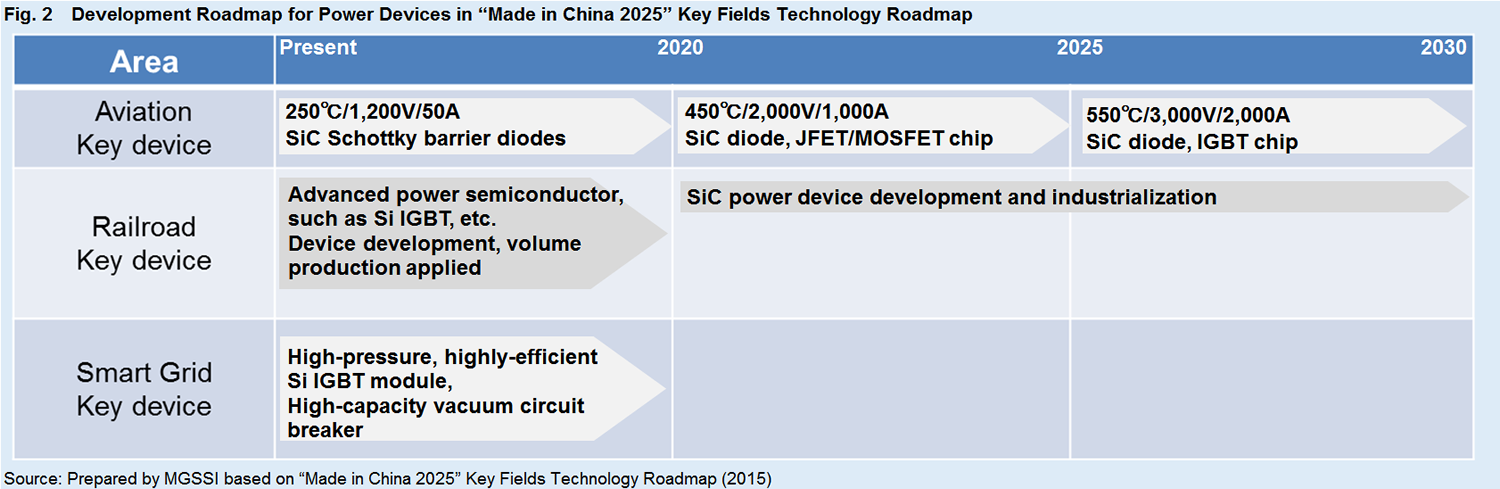

Also, according to the “Made in China 2025” Key Fields Technology Roadmap released in September 2015 (Fig. 2), expected applications of domestic power devices are limited to aviation, railroads, and smart grids. In particular, for volume zones such as railroads and smart grids, development will be limited to Si IGBTs up to 2020, and the next-generation materials, such as Silicon Carbide (SiC), will not be utilized until 2020.

On the other hand, most power device manufacturers in Japan, the US, and Europe are independent companies that do not belong to particular final-product manufacturers, including Infineon Technologies of Germany, Fairchild Semiconductor of the US, and Mitsubishi Electric of Japan. They need to prepare extensive lineups, and as a result, multiple development factors. Furthermore, their development resources are allocated not only to Si devices but also next-generation semiconductors, such as Silicon carbide (SiC) devices. However, the market share of next-generation semiconductors remains between 1% and 2% (2015) because issues relating to manufacturing costs and quality have not been cleared; therefore, next-generation semiconductors have not succeeded in breaking the market dominance of Si power devices yet.

Consequently, Si-IGBT-related technological differences between Chinese manufacturers and Japanese, US and European counterparts are narrowing, and the future development of this technology warrants close attention.

Conclusion and Future Outlook

From the above discussion, in China, in-house production of power devices is becoming a chance to promote domestic production of semiconductor devices.

There are two strategies considered possible after the in-house production of power devices advances. The first strategy is in-house production of semiconductor devices other than power devices. The global market for power devices is worth JPY two trillion, and the market for digital ICs frequently used in smartphones and tablets is valued at JPY 25.2 trillion (Fig. 1). In this area, Huawei and Xiaomi are the leading final-product manufacturers in China. If these manufacturers sought unique specifications in order to differentiate themselves from competitors, and established their in-house design and production of digital ICs no matter how long it might take, China could stop the import drain on its national wealth that it is worried about.

The second strategy is China’s overseas development of power devices. As Zhuzhou CRRC Times Electric has already participated in power device exhibitions in the US and Europe, Chinese manufacturers are gradually broadening their horizons to overseas markets. If Chinese manufacturers were to acquire manufacturing technologies of certain quality, one possible scenario would be that, with Si power devices commoditized in no time, Chinese manufacturers, given their low cost advantages, would drive away Japanese, US, and European manufacturers.

The development of power device manufacturers in China can be viewed as a litmus test for enhancing China’s future semiconductor industry.

- Based on integrated circuit (IS) data. Source: “Made in China 2025” Key Fields Technology Roadmap

- An analog-device type of semiconductor devices. In recent years, semiconductors have become able to control high voltage in excess of 1,000V, thus applied to a wide range of products, such as home appliances, computers, automobiles, etc. The power device is now one of the devices that is indispensable in our daily lives.